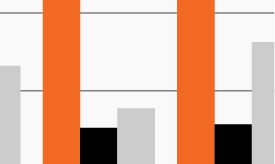

Rolling 1-year Sharpe ratio of 2-year U.S. Treasury note

Source: Bloomberg Finance, L.P., as of September 30, 2022. Sharpe ratio looks at an investment on a risk-return basis.

- Among the long list of volatility drivers since January, rising interest rates have perhaps been the one consistent thread underpinning the highly correlated decline across markets this year.

- The 2-year Treasury yield began the year within shouting distance of its all-time low of 0.78% but has since reached a 15-year high of 4.15%.

- Some investors have welcomed rising yields across government and corporate bonds as they may present an attractive entry point relative to the past several years. Yet, markets also carry notably more volatility. Three of the top five weekly increases in the 2-year Treasury yield have taken place over the past two months.1

- The chart highlights the changing risk-return relationship for the risk-free rate as measured by the Sharpe ratio of the 2-year Treasury. While yields have dramatically increased this year, investors have had to stomach an extraordinarily high level of volatility compared to history. (Sharpe ratio refers to how well an asset’s return compensates an investor for its risk. The higher an investment’s Sharpe ratio, the better its returns have been compared to the amount of risk assumed.)

- Treasuries and core fixed income’s changing risk-return relationships may present a quandary to investors seeking higher yields in what they perceive to be lower risk investments.