Declining income, rising duration leave bond investors vulnerable

Are bond investors prepared for higher interest rate risk? This week’s chart looks at why they may need to seek income and stability from alternative sources.

January 10, 2020 | 1 minute read

Investors and corporations alike have benefited from the low interest rate environment that has prevailed since the financial crisis, and 2019 may have put an exclamation point on this trend.

Investment grade bonds returned nearly 15% last year with returns driven primarily by a peak-to-trough interest rate decline of approximately 120 bps.1 For their part, corporations locked in their debt at lower rates in 2019, issuing just over $1 trillion in new high-grade debt.2

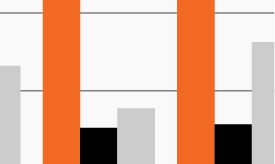

Over the past decade, investment grade corporations also gradually extended the average length of the debt they issued – by nearly 1.5 years in total, from just under 10 years in mid-2009 to nearly 11.5 years as of December 2019.2

Against this backdrop, the average duration of the Bloomberg Barclays U.S. Corporate Bond Index, which measures investment grade bonds’ sensitivity to changes in interest rates, also rose steadily since 2009 and spiked in 2019.2 As the chart shows, it rose by nearly a full year in 2019.2

In other words, as corporations have locked in debt at lower rates and for longer terms, income has declined for investors and they have become increasingly exposed to interest rate risk.

Historically, investors have turned to bonds for their attractive income potential coupled with price stability. Looking forward, however, investors may increasingly need to look outside traditional markets to find both.