See why revenue growth forecasts for the rest of 2018 show a pronounced decline despite a strong projection for Q2.

August 17, 2018 | 1 minute read

The U.S. economy demonstrated its continued strength this week as retail sales data for July came in well above economists’ expectations and showed solid annual growth.1

Corporate earnings reports this year have reflected the healthy economic conditions. For example, Q2 2018 marked the second consecutive quarter of 20%-plus earnings growth and the third consecutive quarter of double-digit earnings growth.2

Yet some analysts believe that Q2 earnings may represent a peak in the current cycle and are more restrained about the prospects for corporate earnings, and economic prospects, in the coming quarters.3

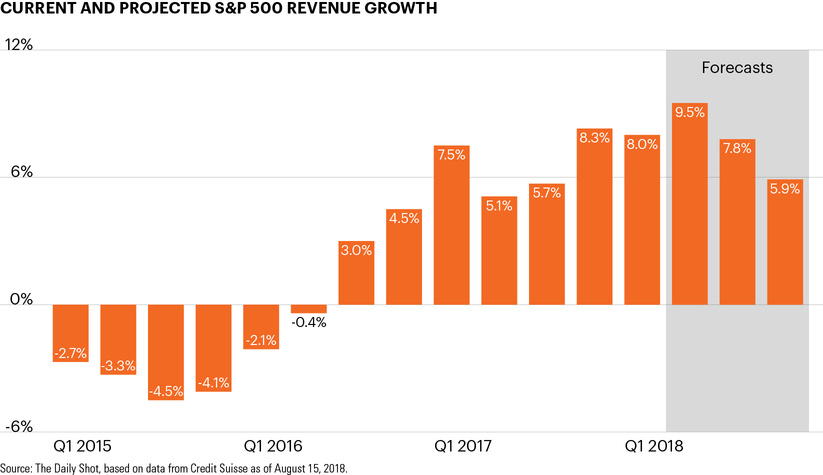

As the chart shows, forecasts for revenue growth, a key component of corporate earnings, of S&P 500 companies show a gradual deceleration in the second half of 2018, from 9.5% in Q2 to just 5.9% in Q4.4 Likewise, the University of Michigan’s measure of current economic conditions sits far above a similar measure of consumer expectations.5

As we noted last week, many of the drivers behind the current, long-running bull market – accommodative central bank policy, ultralow Treasury yields, limited volatility and strong economic tailwinds among them – appear to be shifting. Changing market or economic environments often lead to heightened market volatility as investors adjust to a new environment.