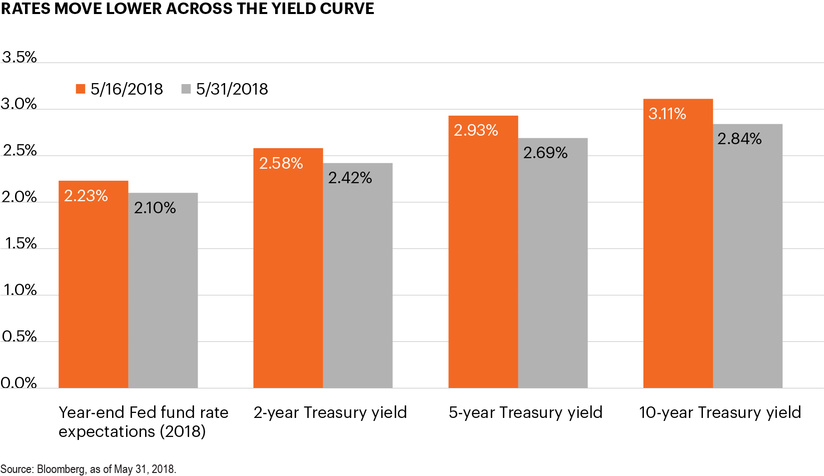

Treasury yields, and Fed fund expectations, decline

Rates move lower across the yield curve

June 1, 2018 | 1 minute read

The 10-year U.S. Treasury yield drew particular interest in mid-May when it reached a four-year high of approximately 3.11%.1 The move seemed to confirm some investors’ fears that interest rates could continue their march higher and run the risk of slowing down economic growth in the United States.

Since its recent peak, however, the 10-year yield fell sharply, approximately 27 bps in just 10 trading days, as investors absorbed a new round of political strife in Italy and Spain.1 At approximately 2.88% on June 1, the 10-year Treasury note is now squarely back into the range in which it has traded through most of 2018.1

As the chart shows, yields across the curve moved lower since reaching their mid-May highs. In the same time frame, market expectations for the target federal funds rate declined approximately 13 bps, or approximately half of one rate hike in 2018, and by a full rate hike (approximately 25 bps) for 2019.2

Investors should not overemphasize the importance of any two-week period. Yet recent declines across the yield curve and Fed funds rate expectations underscore the potential challenges that income-seeking investors could continue to face in 2018 and beyond.

Advisors expect to reduce their clients’ cash allocations this year. Alternatives, multi-asset and real asset investments are among the major beneficiaries.