When will volatility revert to its long-term average?

See how recent market volatility compares to its long-term average and what could drive it higher.

August 24, 2018 | 1 minute read

Despite many potential headwinds, equity markets have remained relatively calm in 2018 while generating a year-to-date return of 8.3%.1

The CBOE Volatility Index (VIX), which measures investor expectations of near-term volatility, spiked in late January over fears that a rapid rise in interest rates might derail the long-running bull market.2 This concern contributed to a U.S. equity decline in both February and March.1

Since then, however, the VIX has been on a gradual downtrend. In 2017, it averaged just 11.1.2 It has stepped up to 15.5 year to date, but both figures are well below its long-term average of approximately 20.7.2

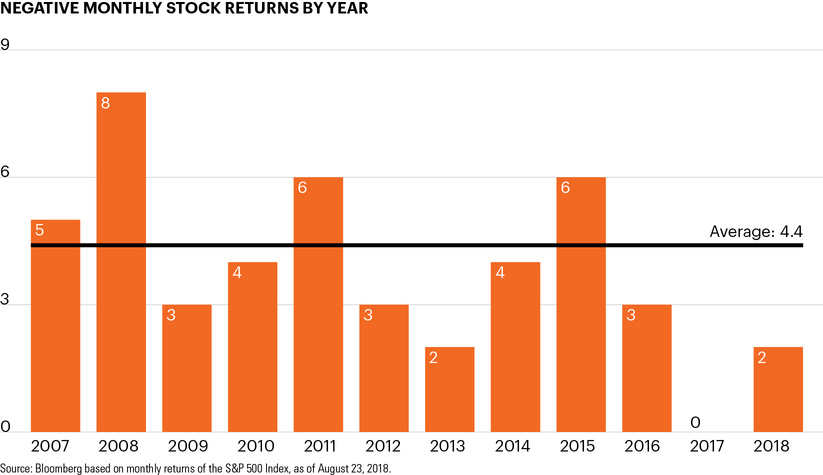

The chart highlights the general disparity in volatility today compared to the longer-term market environment. In the period since January 2017, for example, U.S. equities experienced just two monthly market declines (in Q1 2018) compared to an average 4.4 monthly declines per year in the 10-year period from 2007 through 2016.1

Corporate earnings and economic conditions remain strong, which could help further extend the market’s momentum. As the recently released minutes to the Fed’s July-August meeting highlighted, however, prolonged trade disputes remain among several sources of potential uncertainty and risk.3

Given the current atmosphere, investors may consider preparing for a more traditional level of volatility before it emerges.