See how spreads on corporate bonds have fared over the last 20 years, and why that might point to a prolonged search for income.

September 21, 2018 | 1 minute read

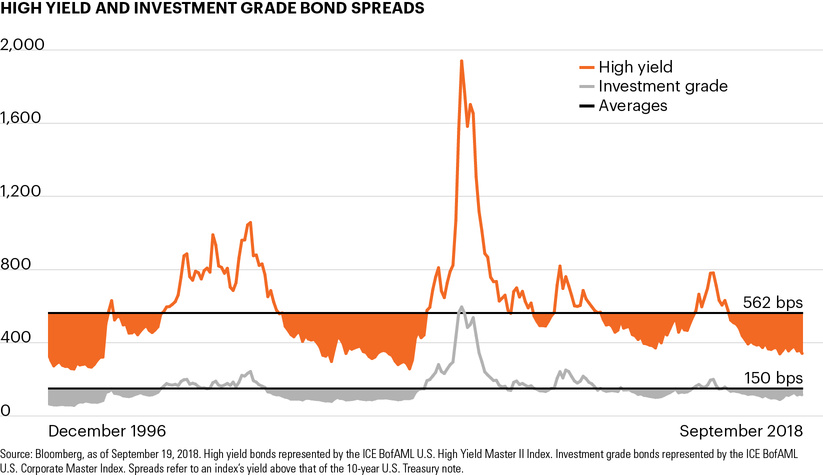

High yield bond prices rose to a near two-month high this week, sending spreads on high yield bonds down to 334 bps, or approximately 228 bps below their long-term average.1 Spreads refer to a bond’s yield above that of risk-free U.S. Treasuries.

Throughout much of the current economic expansion, investors have enjoyed an environment of healthy economic growth, solid corporate profits and a supportive Federal Reserve.

Against this backdrop, spreads on high yield bonds currently reside at their lowest level in more than a decade.1 As the chart shows, however, periods of tight credit spreads are not uncommon. Spreads on both high yield and investment grade bonds have spent long periods of time below their long-term averages over the past 20 years, most notably between approximately December 2003 and December 2007.1

Both corporate fundamentals and the broader U.S. economy remain strong and are supportive of an environment in which corporate credit yields remain at or near long-term lows.

Despite the fact that the Fed has raised rates seven times since December 2015, finding high levels of income among traditional fixed-income asset classes continues to be challenging in today’s market.2

Private credit has increasingly become the preferred source of financing for PE sponsors, with direct lending volume jumping 60% over last year’s level.