Payrolls rose 211,000 in April, recovering from the big downside surprise in March of only 79,000 new jobs. Strong payrolls have helped fuel investors’ expectations for future U.S. growth, and that sentiment is well reflected in rising equity markets. We believe investors would be wise to take a more grounded view and recognize that the economy can only grow as fast as labor force growth and productivity allow. As investors’ growth expectations rise, we believe payrolls will likely function more like a ball and chain than a catalyst for growth.

High hopes and strong payrolls

Expectations about the economy have improved markedly in the first quarter of 2017, and strong payrolls have been playing their part. This optimism is apparent in a wide variety of indicators. For example, consumer and business sentiment indicators have risen significantly in the first quarter, with several indexes at or near decade highs.¹

But against the backdrop of confidence in future growth, we believe markets have started taking strong payroll gains for granted. During this expansion, we have seen the longest stretch of uninterrupted payroll increases since the Bureau of Labor Statistics began tracking the data in 1939. Moreover, job gains have been steady and strong, with the 12-month average hovering between 180,000 and 220,000 for five years.²

Yet the current pace of payroll gains will be difficult to maintain. Adding more than 16 million jobs² since the recession ended has pulled the unemployment rate down from 10.0% in 2009 to 4.4% in April.³ That is below the Fed’s estimate of full employment⁴ and indicates that the labor market will soon run low on unemployed people to pull into the labor force.

So it really isn’t the market’s fault. When you have been lulled into thinking anything below 180,000 is a downside surprise, it is easy to forget that official estimates of “trend” payroll gains are closer to 75,000.⁵

Growth is all about payrolls

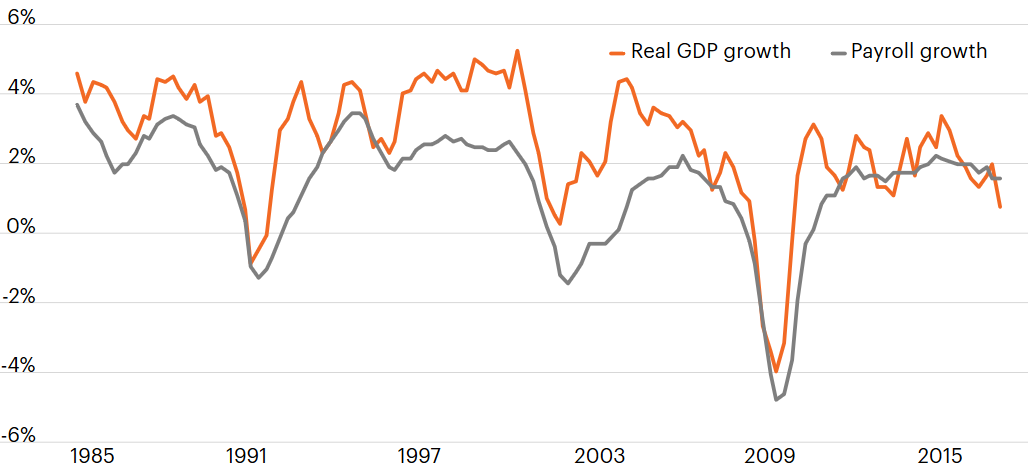

More so now than at any other time since the 1970s, growth in our economy is directly linked to growth in employment. The two strongly trend together, as can be seen in the chart below, with employment rising and falling with the business cycle (albeit with a lag). Historically, the economy typically grows at a faster rate than employment gains. During the expansion in the 1990s, GDP averaged 3.5% while employment growth averaged 1.9%. In the expansion during the 2000s, GDP averaged 2.6% while employment growth averaged 0.7%. However, over the last five years GDP growth of 2.1% has barely outpaced employment growth at 1.8%.⁶

Strongly linked: Growth of GDP and payrolls year over year

Sources: Bureau of Economic Analysis, FS Investments.

What’s changed? The big difference today is that productivity growth is close to zero in our economy. Productivity peaked in 2004 and has been on a downtrend ever since, averaging only 0.6% over the past five years.

Growth in productivity – each individual worker creating more output – is critical because without it, more growth is entirely dependent upon more workers. Put another way, the upside to growth is limited by the pool of available labor, which was deep right after the recession ended, but with every strong payrolls report is rapidly becoming shallower.

Moderating payrolls could stifle growth expectations

Positive growth expectations have raised hopes that businesses may increase investment spending and that infrastructure spending could further boost output. But after years of strong employment gains, the unemployment rate is already signaling that additional labor may be hard, and more expensive, to find.

The link between economic growth and job growth is strong. Without productivity growth, the link turns into the proverbial ball and chain, where scarce labor resources could stifle growth. But if payroll gains moderate over the coming year, as we expect they will, we could see markets face a painful adjustment as potential growth remains constrained at current low levels.