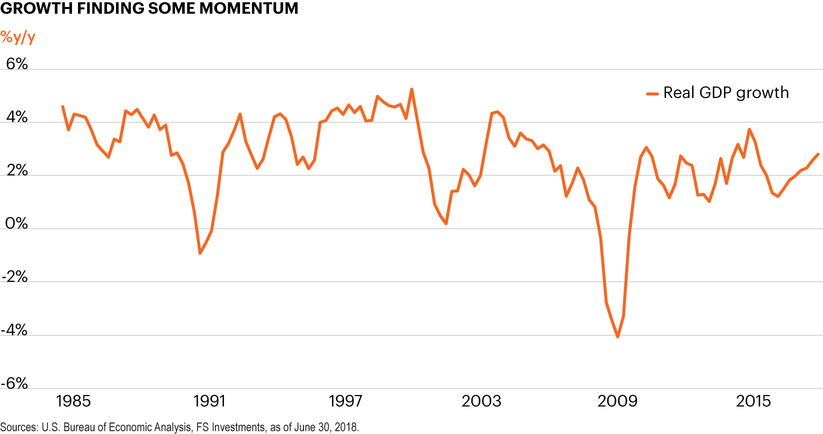

Real GDP growth has trended lower over the last 50 years, caused primarily by slowing labor force growth and productivity. Positive cyclical momentum caused growth to pick up in the second half of 2017 and the first quarter of 2018, and optimism is high that the rest of 2018 will see a further boost from pro-growth policies. Yet the gravitational pull of structural headwinds is powerful, and over the long term we believe investors may need to prepare their portfolios for a lower-for-longer growth environment.

Economic indicators

To gauge whether the recent state of positive growth data is cyclical or structural in nature, we are monitoring the following:

Risk of recession?

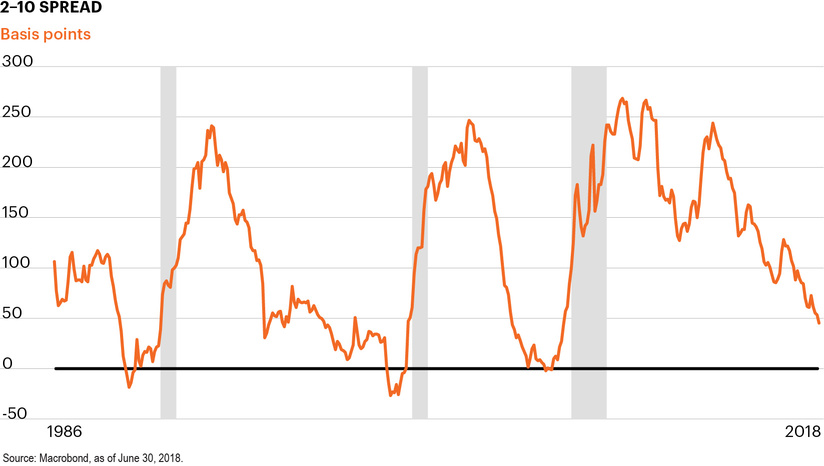

The shape of the yield curve, as represented by the spread (or difference) between the 2-year and 10-year Treasury rates, has been an important indicator of past recessions.

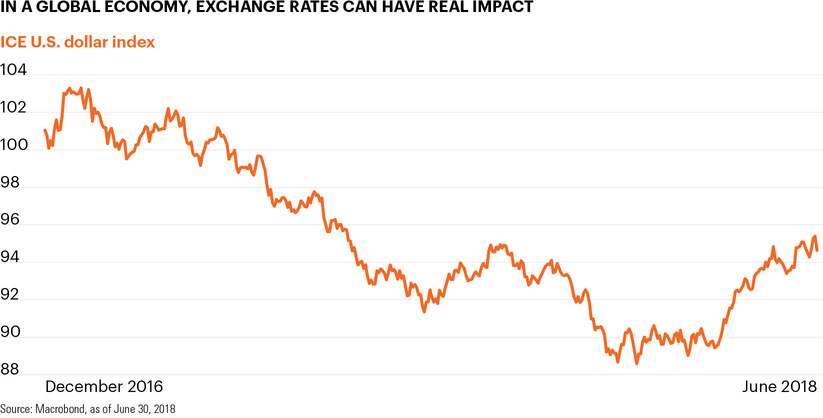

U.S. dollar

One oft-overlooked factor in the U.S. growth landscape is the relative strength of the U.S. dollar. A commonly watched measure of the dollar’s value is the ICE U.S. Dollar Index, which compares the dollar versus a weighted average of other major global currencies, including the euro and the Japanese yen. All else equal, a strengthening dollar acts upon the economy much the same way rate hikes do, in part by slowing U.S. growth as our exports become less competitive. Shifts in exchange rates can also have a major impact on the earnings of multinational U.S. companies and thus bear watching.

We will be watching: In 2017, U.S. multinational corporations reaped the benefits as the dollar index plunged almost 10%. As a result, S&P 500 companies with relatively high foreign revenue exposure outperformed companies that have high domestic revenue exposure by 14.8% for the year.1 Most companies have currency hedges in place, but they are designed to overcome short-term changes in exchange rates. If the dollar continues to strengthen – a realistic possibility given that interest rates in the U.S. continue to be attractive versus other developed nations – companies that rely on domestic operations would be expected to outperform.

Risks to our view: We do not have a specific view on this subject. But the foreign exchange market remains one of the most volatile, and there are real risks to the economy if we see large swings in exchange rates. Similarly, if severe dollar weakness that has dislocated from underlying macroeconomic fundamentals materializes, it bears closer analysis and could signal other issues at work.

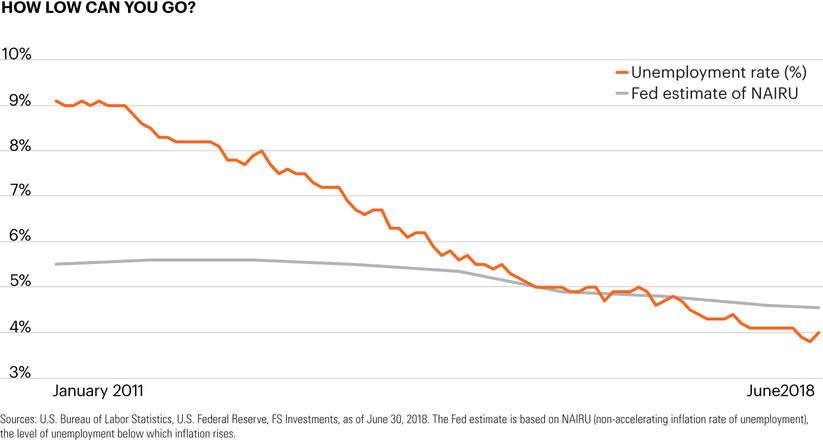

Unemployment rate

The economy added over 2.3 million jobs in the past year, and this breakneck speed of employment gains pulled the unemployment rate down from 4.3% in May 2017 to 3.8% by May 2018.2 The challenges imposed by long-run demographic trends have not changed, however, and the labor market could increasingly be a headwind for growth in more ways than one.

We will be watching: The monthly payroll report has been front and center of the economic landscape again in 2018. In particular, the unemployment rate has now moved well below the Fed’s long-run equilibrium estimate. As the labor market continues to boom, the Fed has been forced to continuously revise down its unemployment rate projections; at its June meeting, the Fed projected the jobless rate to be 3.6% in 2018, down from 3.8% at the March meeting. For the first time since the Department of Labor started tracking data in 2000, the number of total job openings is greater than the number of unemployed persons.2 Considering this, we will be watching to see whether the economy can continue its pace of adding close to 200,000 jobs per month.3

Risks to our view: So far, the Fed has shown little concern about the tightening labor market and has continued its slow, cautious pace of rate hikes. However, it remains to be seen if the Fed will tolerate an unemployment rate increasingly beyond its own estimate of equilibrium. An unemployment rate below 3.5% could shift the Fed rate hike cycle into a higher gear.

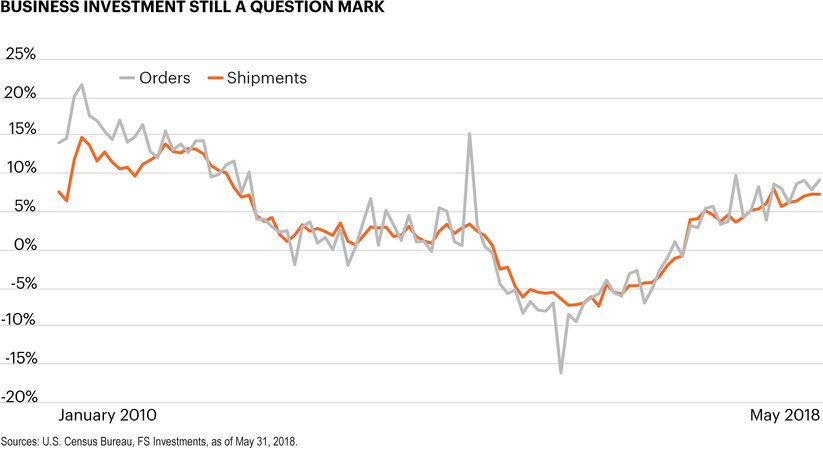

Business investment

Productivity growth has been trending downward since 20044 and is a significant contributing factor to today’s low-growth environment. There is a wide range of theories as to why productivity is in secular decline. Weak business investment, which has underperformed during this expansion, is an obvious culprit holding back a productivity-related boost to potential output. Productivity growth would have to recover for several years to return to the 2.2% trend seen from 1950–2000.5

We will be watching: Monthly durable goods orders and shipments data offer a timely indication of whether businesses are investing in capital equipment. The Tax Cuts and Jobs Act has cut the corporate tax rate from 35% to 21% and altered tax-exempt timing on depreciation to incentivize investment spending. This lineup of pro-business news has created a swell of anticipation that business spending will improve markedly.

Risks to our view: Uncertainty related to international trade agreements and potential tariffs has spiked, which could put investment plans on hold for companies with international supply chains and international revenue flows.

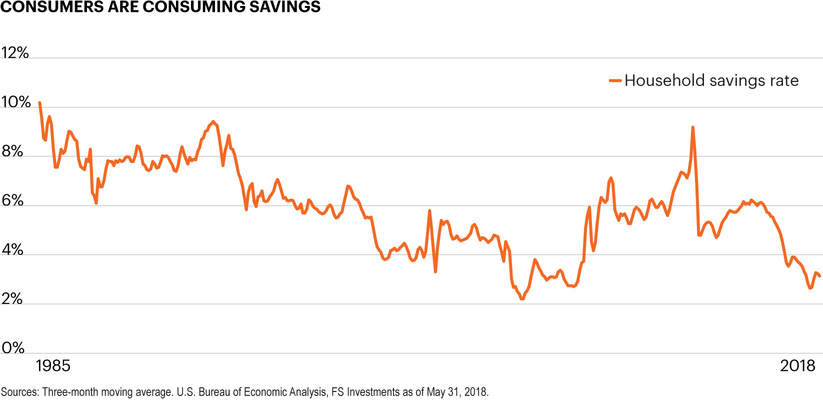

Savings rate

Against a historically low-growth environment, consumers stand out as the engine of the U.S. economy. Consumption accounts for 69% of U.S. growth and is supporting most aggregate demand and revenue generation in the economy.6

We will be watching: The household savings rate shows savings as a share of personal disposable income. The current level is below that of the previous 1991–2001 expansion and is closing in on all-time lows seen in 2005. Consumers remain a vital, positive contributor to economic growth, but sluggish wage growth has caused consumers to finance spending by dipping into savings. Positives such as a tight labor market and solid equity market performance have buoyed consumers for several years, but a more volatile market without significant wage gains could cause consumption to face headwinds going forward.

Risks to our view: Consumers may disregard the low savings rate and keep on spending, leveraging themselves back to levels seen before the Great Recession. This could create risks should interest rates rise significantly or should the economy eventually slow again.

Risk of recession?

Slower growth should not be confused with a recession. There is a big difference between slower growth and no growth. The U.S. economy is experiencing positive growth momentum, and pro-growth policies are set to drive growth above current levels in coming years. However, in the interest of education, investors can easily follow this indicator, which is a key ingredient of almost every academic model that attempts to predict recessions. The shape of the yield curve, as represented by the spread (or difference) between the 2-year and 10-year Treasury rates, has been an important indicator of past recessions.

We will be watching: As can be seen in the above chart, yield curve inversion (when long-term interest rates are lower than short-term interest rates) is often seen as a signal of an impending recession. Even as the Fed has consistently raised short-term rates, the longer end of the curve remains stubbornly range-bound. On June 27, the 2–10 Treasury spread hit 32 bps, the narrowest it has been since 2007. We will continue to watch the shape of the yield curve closely as it has a high correlation to impending economic stress.

Risks to our view: The risk of a recession could rise if the Fed sees inflation start to pick up and becomes more aggressive in its rate hike path. This scenario is generally described as a classic Fed “overshoot.”

Learn more

Declining long-run potential growth, contained inflation expectations, and low global yields have all put downward pressure on interest rates for years. Interest rates peaked in the high inflation days of the 1980s, and today’s lower rates mean investors have fewer options to meet their income needs.