Breakdown of Barclays Agg total returns over time

Source: ICE BofAML U.S. Corporate Index, ICE BofAML U.S. High Yield Index, S&P/LSTA Leveraged Loan Index. Based on rolling 10-year data ended September 24, 2021. Duration measures the sensitivity of a bond’s price to changes in interest rates. Empirical duration uses historical data to calculate the observed change in a bond‘s price given changes in rates. It is calculated regressing weekly change in high yield bond index prices and weekly change in 5-year U.S. Treasury yields.

- Treasury yields have risen sharply since the Fed adopted a more-hawkish tone at its September meeting. Since September 22, the 2-year Treasury yield has risen as much as 6 basis points while the 10-year yield jumped 22 basis points before both moderated a bit.1

- Amid the rising rate environment, core fixed income returns have suffered. The Barclays Agg returned -0.87% in September, bringing its YTD return down to -1.55%. Over the same time, credit markets have held up relatively well. High yield bonds are flat in September while senior secured loans are up 0.64%. Year to date, they have returned 4.7% and 4.4%, respectively.2

- The divergent paths illustrate the varying degrees of duration risk across fixed income asset classes. (As a reminder, duration measures the sensitivity of a bond’s price to changes in interest rates).

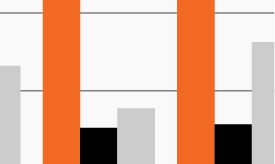

- To this end, the chart compares stated duration to empirical, or observed, duration. Stated duration is based on a preset formula while empirical duration uses historical data to calculate a bond’s sensitivity to changes in interest rates.

- Over the last ten years, the duration of high yield bonds and senior secured loans has been lower than investment grade corporate bonds, as most would expect.2 Looking at empirical duration tells a more complete story of their relationship to interest rates. In fact, high yield bond and senior secured loan prices increased approximately 1.4% and 2.6%, respectively, for every 100-basis point increase in interest rates over the last decade.2

- At a time when many investors are looking to reduce or diversify their interest rate risk, below-investment-grade bonds may be particularly attractive against the backdrop of generally stable economic conditions, an uncertain interest rate outlook and expectations for the Fed to begin tapering.